7 Reasons the FTA May Audit Your Business in the UAE

Many business owners still believe that tax audits happen randomly.

That may have been true years ago in some countries, but today the UAE Federal Tax Authority has access to far more information than most businesses realise. VAT returns, Corporate Tax filings, customs data, banking information, and financial statements can all be compared and analysed.

This does not mean that every business will face an audit. However, certain patterns and compliance gaps can make your business stand out.

Here are some of the issues we commonly come across when reviewing client records.

1. Your VAT Return Tells a Different Story Than Your Accounts

This is perhaps the most common issue.

We often see businesses filing VAT returns based on one set of figures while their accounting records show something completely different.

Sometimes it happens because entries were passed after the VAT return was filed. Sometimes it is simply due to poor bookkeeping.

Whatever the reason, if the revenue reported to the FTA does not match the revenue appearing in your financial statements, it is likely to raise questions sooner or later.

A VAT return should never be viewed as a separate exercise. It should always tie back to the books.

2. Missing Documents

A client may tell us that an expense is genuine.

That may be true.

The problem is that during an audit, the FTA is not interested in explanations alone. They want supporting documents.

- No tax invoice.

- No contract.

- No import document.

- No supporting evidence.

In many cases, that is where the problem starts.

We have seen businesses lose valid VAT claims simply because the paperwork could not be produced when requested.

3. Corporate Tax Positions With No Supporting File

Corporate Tax is still relatively new in the UAE, and many businesses are focusing only on filing the return.

The return itself is only part of the process.

The real question is whether the business can support the figures if the FTA asks for clarification later.

For example, if a company claims a large expense deduction, can it demonstrate why the expense was incurred and how it relates to the business?

If a Free Zone company claims tax benefits, does it have the records to support its position?

These are questions businesses should be asking now rather than during an audit.

4. Consistently Missing Deadlines

Everyone misses a deadline occasionally.

However, repeated delays in registrations, tax filings, or payments can create a poor compliance history.

From a regulator's perspective, repeated non-compliance may indicate weaknesses in internal controls.

Apart from penalties, it may increase the likelihood of future scrutiny.

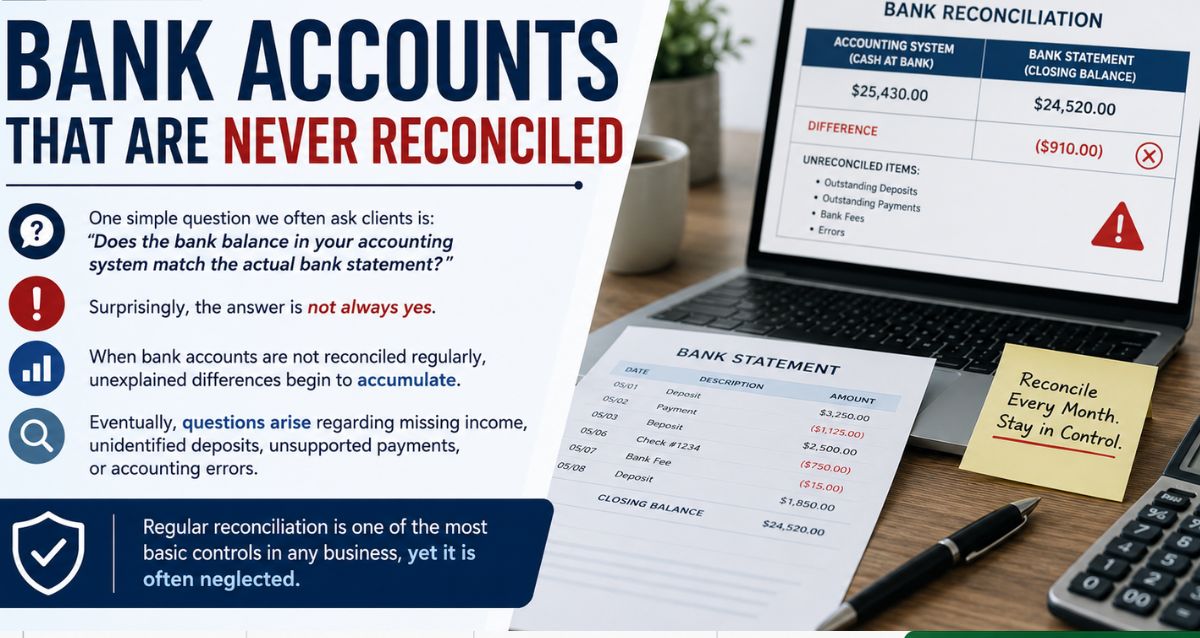

5. Bank Accounts That Are Never Reconciled

One simple question we often ask clients is:

"Does the bank balance in your accounting system match the actual bank statement?"

Surprisingly, the answer is not always yes.

When bank accounts are not reconciled regularly, unexplained differences begin to accumulate.

Eventually, questions arise regarding missing income, unidentified deposits, unsupported payments, or accounting errors.

Regular reconciliation is one of the most basic controls in any business, yet it is often neglected.

6. Related Party Transactions With No Documentation

Since the introduction of Corporate Tax, related-party transactions have become an important focus area.

Many businesses transfer funds, charge management fees, share resources, or provide services between group companies without proper documentation.

The transactions themselves may be legitimate.

The issue is proving that they were carried out on commercial terms and properly recorded.

Without documentation, even genuine transactions can become difficult to defend.

7. Shareholder Withdrawals That Are Not Properly Recorded

This is particularly common in owner-managed businesses.

- A shareholder withdraws funds from the company.

- A director introduces money into the business.

- Payments move through current accounts.

- None of this is unusual.

The problem arises when there is no clear record explaining what happened.

- Was it a loan?

- Was it additional capital?

- Was it repayment of an earlier amount?

If the paperwork is missing, these transactions can attract unnecessary attention during a review.

The Best Time to Fix Compliance Issues

Unfortunately, many businesses start reviewing their records only after receiving a notice from the FTA.

By then, the pressure is already on.

- Documents need to be located.

- Transactions need to be explained.

- Old reconciliations need to be completed.

What could have been addressed gradually over several months suddenly becomes urgent.

That is why we always recommend periodic compliance reviews instead of waiting for an audit notice.

How Can Flyingcolour Tax Consultants Help?

At Flying Colour Tax Consultants, we regularly assist businesses with VAT reviews, Corporate Tax compliance checks, audit preparedness assessments, transfer pricing documentation, accounting support, and FTA audit assistance.

Our objective is simple.

Identify potential issues before the regulator identifies them.

In many cases, a few corrective actions taken today can prevent significant penalties and disruption tomorrow.

Final Word

Most tax audits do not begin because a business deliberately made a mistake.

More often, they begin because records are incomplete, figures do not reconcile, or documentation is missing.

The businesses that generally face fewer problems are not necessarily the largest ones. They are the ones that maintain proper records, review their compliance regularly, and address issues before they become serious.

In tax compliance, prevention is usually far less expensive than correction.

FAQ

Q. Why would the FTA flag my business if my VAT returns are filed on time?

Filing on time doesn't protect you if the figures don't match. The most common trigger is a mismatch between what's reported on the VAT return and what actually appears in the accounting records, often because entries were posted after the return was filed or bookkeeping wasn't kept current.

Q. What happens if I can't produce documents for a valid expense during an audit?

Even genuine expenses can be disallowed if there's no tax invoice, contract, import document, or other supporting evidence. The FTA works from documentation, not explanations, so businesses can lose otherwise legitimate VAT claims simply because the paperwork wasn't available when requested.

Q. Is filing a Corporate Tax return enough, or do I need supporting documents too?

Filing is only the first step. The FTA can ask a business to justify any position later, such as why a large expense deduction was incurred or why a Free Zone company qualifies for the tax benefits it claimed, so the underlying file needs to support the return.

Q. Does missing a single tax deadline put my business at risk?

A one-off delay is unlikely to cause issues, but repeated late registrations, filings, or payments build a poor compliance history. Regulators can read repeated non-compliance as a sign of weak internal controls, which raises the likelihood of closer scrutiny later.

Q. Why does bank reconciliation matter for tax compliance?

When the bank balance in your accounting system doesn't match the actual bank statement, unexplained differences accumulate over time. These gaps eventually raise questions about missing income, unidentified deposits, or unsupported payments, even when there's a simple explanation behind them.

Q. Do related-party transactions need formal documentation even if they're legitimate?

Yes. Since Corporate Tax was introduced, transactions between group companies, such as management fees or shared resources, need to be properly recorded and shown to be on commercial terms. Without documentation, even fully legitimate transactions become difficult to defend.

Q. How should shareholder withdrawals and director contributions be recorded?

Every withdrawal or capital injection needs a clear record stating whether it was a loan, additional capital, or a repayment. Movements through current accounts without paperwork explaining their nature often draw unnecessary attention during a compliance review.

(SSK)*

To learn more about 7 Things That Could Put Your Business on the FTA's Radar, book a free consultation with one of the Flyingcolour team advisors.

Disclaimer: The information provided in this blog is based on our understanding of current tax laws and regulations. It is intended for general informational purposes only and does not constitute professional tax advice, consultation, or representation. The author and publisher are not responsible for any errors or omissions, or for any actions taken based on the information contained in this blog.